Factor trends, value, personal finance and Tian Yang - the best investing blogs and podcasts from the past week

Factor trends, value, personal finance and Tian Yang - the best investing blogs and podcasts from the past week

There’s an interesting accepted truth in investing that shares in ‘small’ companies tend to outperform shares in large companies.

That is to say, all things being equal, smaller stocks do better than big ones on average.

It’s certainly the case that many strategies and plenty of investors obsess about small companies.

But the funny thing about the size effect (the observation that small beats big) is that soon after it was identified by a guy called Rolf Banz in the early 1980s, it stopped working. And it hasn’t really worked since.

Academic and professional studies into this have reached a loose conclusion for now that you can explain away the size effect. For a start, smaller company shares tend to have higher sensitivity to the market (ie. beta), so they’re capable of doing better just from the market return.

There’s also a case to say that when you throw in additional factors like value and momentum (ie. they’re either cheap or trending higher) you get a punchier return from smaller stocks than big ones - and that explains what appears to be a size effect. You can read more about this in places like Alpha Architect and AQR.

I’ve mentioned this before, but another slightly complicating issue for UK investors (or perhaps just any investor outside of the States) is that ‘small’ means something slightly different in the US. ‘Small’ there means $300 million to $2 billion. ‘Small’ here can mean anything from £20 million upwards.

So buying a small-cap in the UK and expecting it to behave like the small-caps you read about in US factor investing research might be a mistake.

Anyway, this brings me to a recent research paper by Andrew Ang, the head of factors, sustainable and solutions at the investing giant, BlackRock.

Despite being published publicly, it’s covered in alarming disclaimers (so I’ll leave you to make your own decisions about that). The paper is here and it’s called Trends and Cycles of Style Factors in the 20th and 21st Centuries

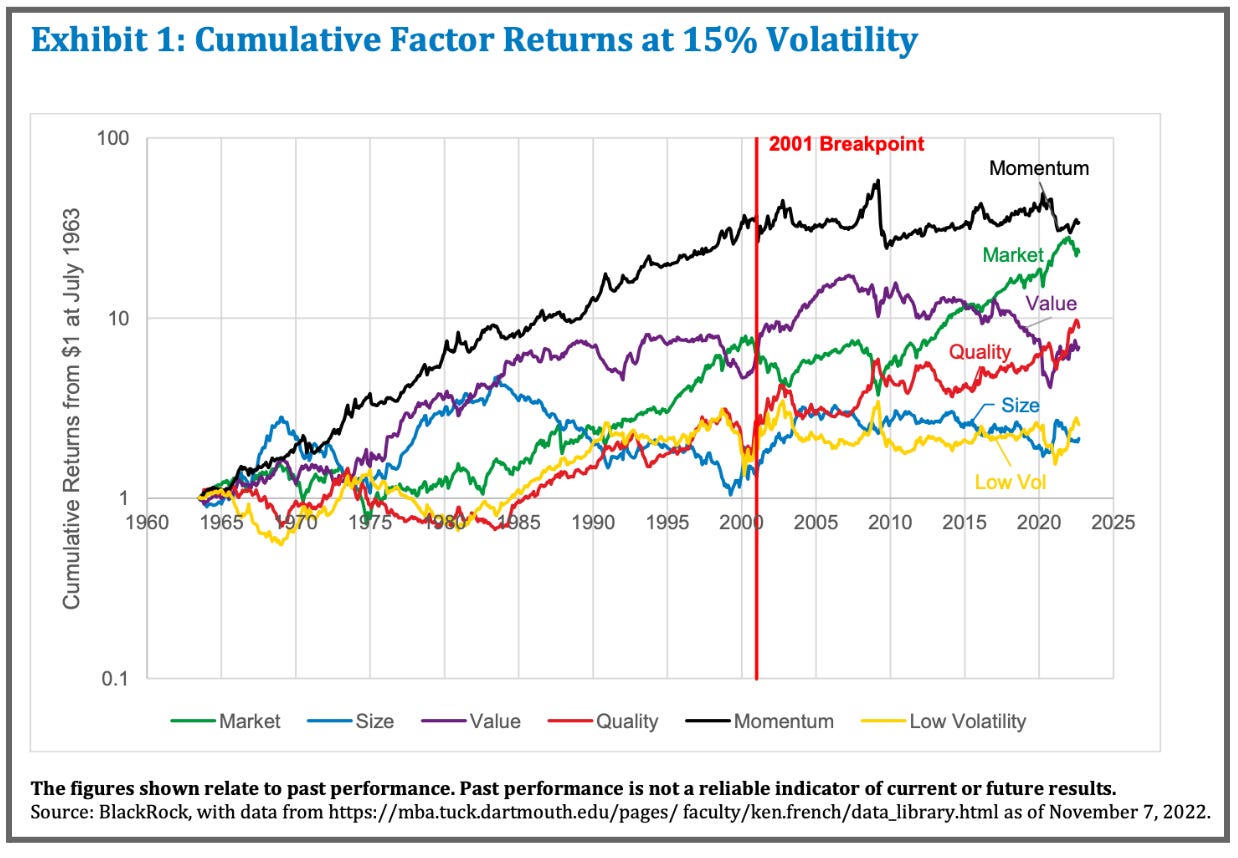

This is a very cool study for anyone interested in how factors have performed since the mid-1960s. As you can see from this chart, the size effect has played very little role in driving returns.

Up to and including the year 2000, momentum and value were very dominant. But things changed in the early years of the new century. Previously high flying factors flattened out, or went south in the case of value. In their place, market return played a central role (bear in mind the US-centric data) and quality came to the fore, too. Low volatility has been flat over the past 20 years, but had a strong year in 2022.

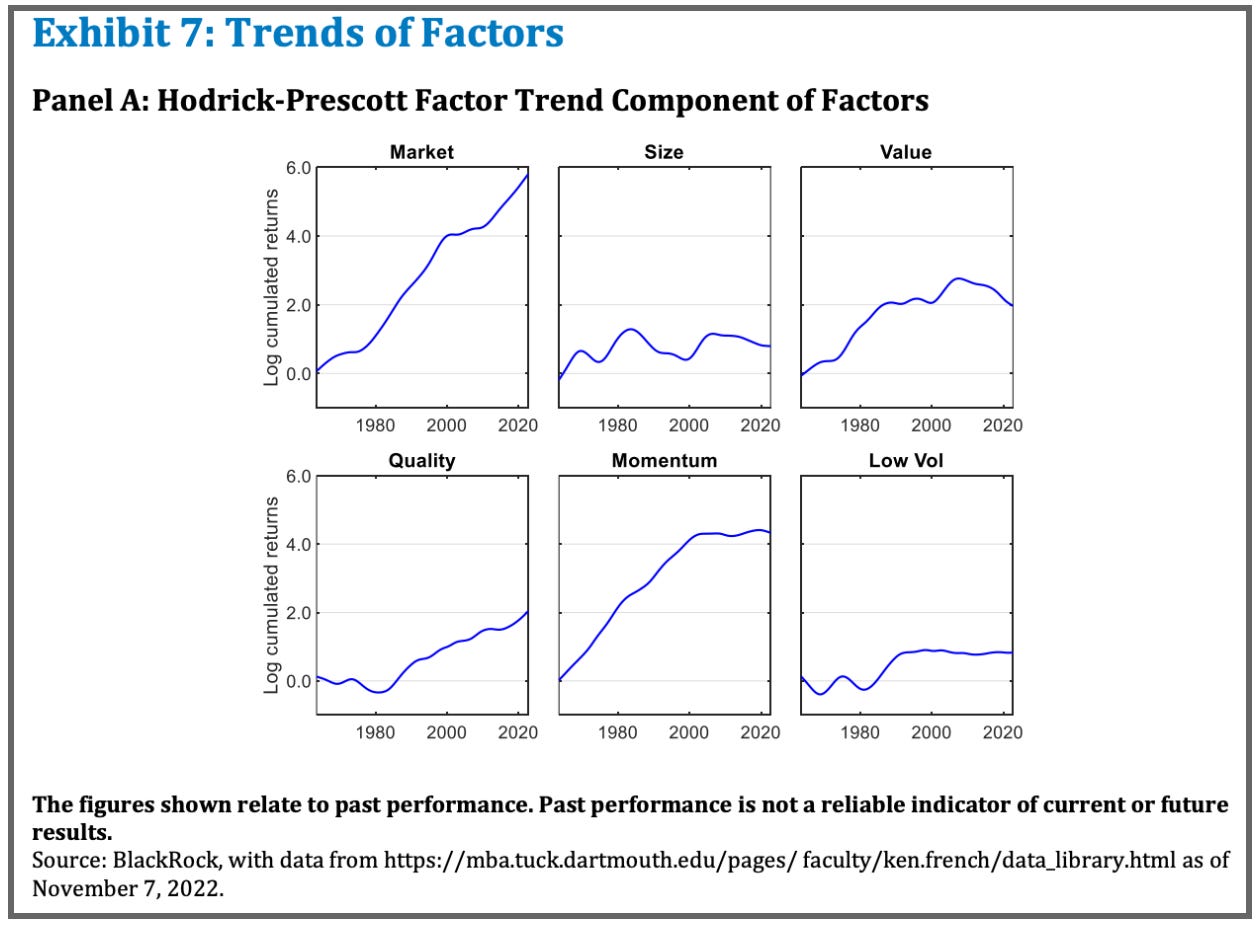

Here’s a slightly different view. Ang uses the Hodrick-Prescott acts to smooth out the trend by removing shorter-term cyclical fluctuations. It shows how the market return has easily been the consistently dominant factor over time - and that quality is in the ascendancy.

Highlights from the past week

Merryn Talks Money, Bloomberg - The Year of the Value Hunter Has Arrived

Merryn Somerset Webb gets some really good people on her Bloomberg podcast. I was going to cover a recent episode with Russell Napier (which you can find here) but I’ve gone with this one instead with Ben Inker from the US value-focused asset manager, GMO.

GMO is very value focused and a lot of their recent research covers the nature of bubbles - which is understandable because markets haven’t worked for their strategies for more than a decade. The Covid years and the 2022 sell-off presented an unusual set of circumstances that don’t easily fit with the models of how value tends to come in and out of favour.

The conversation takes a look at the pain of getting caught out by value traps and growth traps, last year’s blow out of speculative assets and spluttering return of value. One of the unusual features last year was that value did relatively well but ‘deep value’ didn’t work as expected. That means US deep value stocks are extremely cheap, but the S&P is still expensive. It’s a complex picture. Overall, Ben reckons that the bear market isn’t over but that value is still relatively cheap, which bodes well for the coming year.

Tim Harford - What economists get wrong about personal finance

Slightly unrelated to this article by Tim Hartford, I saw something this week by Ben Carlson about some of the things he’s learned from writing an investment blog for the past 10 years (here). He mentions the fact that he’s concluded that “personal finance is more important than investing”. Or to put that another way, if one were the cart and one were the horse, personal finance ought to be the one with four legs. Implicit in that is the point that you could be a truly great stock picker and still struggle if your personal finances aren’t optimised.

This article by Tim Hartford riffs on the same idea. He picks up on research showing that the advice of finance academics isn’t always in harmony with what personal finance gurus say in the millions of books that they sell. Sure, some things they agree on. But most things they don’t. And that brings us to the broader point that standard economic advice often gets things wrong and doesn’t really make allowances for the radical uncertainties of life or of human nature.

Behind the Balance Sheet - Episode 20 - The Data Scientist

This conversation restored my faith in podcasts this week. Having listened to over an hour of something completely different elsewhere (and written it up) I scrapped it because I realised the whole thing was as dull as dishwater. Which just goes to show that you can get seemingly first class guests and still end up with something underwhelming.

This, on the other hand, is great. It’s Stephen Clapham talking to Tian Yang, who runs a macro advisory firm called Variant Perception (@VrntPerception).

His view of investing is very quantitative, and he views it through two lenses of ‘fundamentals’ (a handful of axioms, or absolute facts) and ‘playing the game’ (which is what most investors spend their time doing). He looks at a few key metrics in company financials to try and understand where they are in the capital cycle (the theory of how businesses work in the real world). Really that’s about understanding whether a company’s asset base is growing or shrinking and how its returns are changing.

It’s interesting hearing Tian talking about different types of macro data (like employment stats), how often it’s revised and how careful investors have to be with it. But generally, for a quant-driven view of macro trends and theories about how the world is developing, this is worth a listen.

Have a great weekend!

Ben

Thinking & Strategy

Investing Matters

[Podcast] Episode 34 - Andy Brough, Head of Pan-European Small and Mid-Cap Team, Schroders

Neckar Substack

The 'Berkshire System': Life Advice From a Shareholder Letter

Klement on Investing

News vs. sentiment

The lethargy of large caps

Aswath Damodaran / Musings on Markets

Data Update 5 for 2023: The Earnings Test

Institutional Research

Liontrust

The multi-trillion-dollar conundrum

Man

The Road Ahead: Lessons From the 1970s

Verdad

Risk Eats Return

Larry Swedroe / Alpha Architect

Factor Returns and the Information in Valuation Spreads

Morgan Stanley / Consilient Research

A Practical Guide to Measuring Opportunity Cost

Amundi

Why and what if inflation falls faster than expected?

Finominal

What's My International Exposure?

Securities & Markets

Maynard Paton

[SharePad] Screening For My Next Long-Term Winner: TELECOM PLUS

Investment Masters Class

Learning from IKEA’s Ingvar Kamprad

Fund research from Trustnet

FTSE 100 breaches 8,000 for the first time as UK stocks march higher

AJ Bell Money & Markets

[Podcast] Inflation double whammy, Barclays disappoints, Premium Bond boost and investor stories

TWIN PETES INVESTING

Podcast no.94 with LIVE in person video

Investors' Chronicle

[Podcast] The Companies and Markets show: BP & Shell's bumper profits, Unilever, housebuilders

Money Makers

[Podcast] Weekly Investment Trust Podcast with Jonathan Davis (11 Feb 2023)

Quality Small Caps

[Podcast] Small Caps Podcast with Paul Scott – Episode 6 for 2023