Factors are back, forecasts, Dan Rasmusson and stock picking...

Factors are back, forecasts, Dan Rasmusson and stock picking...

The best investing blogs and podcasts from the past week

When it comes to understanding what may or may not be appealing about different shares, it can be really helpful to divide the stock market into a collection of buckets.

For sure, some shares won’t deserve a place in any of those buckets. And others will fall into more than one. But creating buckets in the stock market can help you understand what you’re really dealing with.

All this, of course, is a rather simplified description of ‘factor’ investing. To put it another way: there are well-studied ‘premiums’ out there that have been linked with above-average performance over time (but not all the time). These are some of the best known premiums (buckets):

Value (undervalued shares tend to do better than expensive ones)

Quality (shares in companies that are good at generating strong cash profits tend to do better than unprofitable ones)

Size (shares in smaller companies tend to achieve stronger returns than those in large companies)

Momentum (strong medium-term price trends tend to persist for a time)

Volatility - or Beta (shares that are relatively less volatile and less sensitive to market moves do better over time)

These are the basics but there are many more.

Buckets like these make the stock market much more relatable to the average investor. Whether you prefer your equity exposure to be handled by fund managers, index funds, or you like to get hands-on yourself, this kind of mental model makes sense of the market.

But what academic finance has given 21st century investors, it also likes to take away. A few of the personalities involved in studying, developing (and profiting) from these ideas, like to cross swords sometimes.

Back in 2016, industry heavyweight Rob Arnott (founder of Research Affiliates) wrote a paper called “How Can ‘Smart Beta’ Go Horribly Wrong?” (at the time, ‘smart beta’ was marketing speak for factor investing and has since largely disappeared).

He irritated a few people with that paper, including rival academic/billionaire Cliff Asness of AQR Capital. It led to ridiculous headlines like this:

Anyway, it all blew over. But Arnott is back with an update on his 2016 paper called: Revisiting Our “Horribly Wrong” Paper: That Was Then, This Is Now

Indulgent? Maybe

Trying to prove a point? Probably

Interesting? Absolutely…

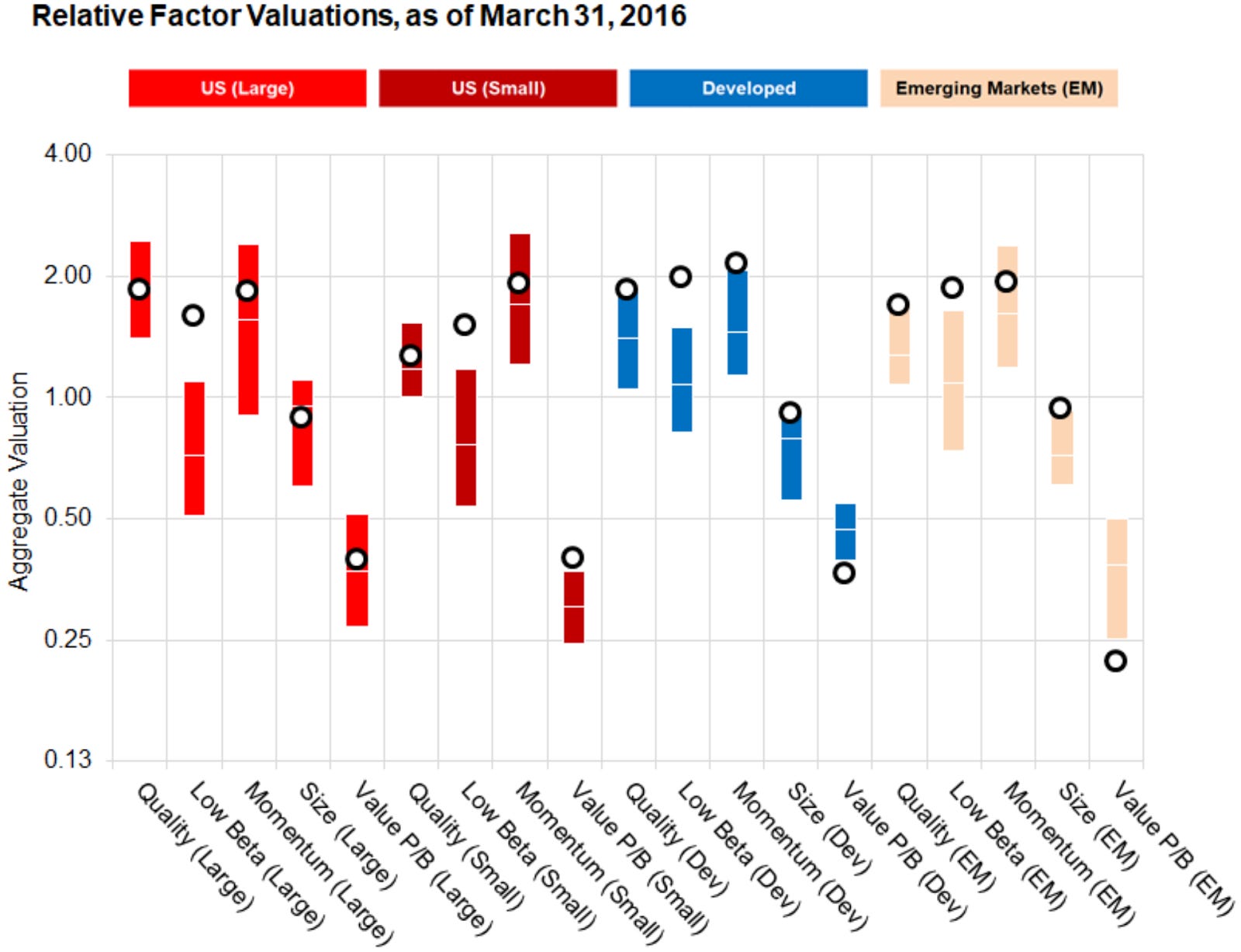

Among other things, this new Research Affiliates study looks at the changing ‘valuation’ of different factor premiums since the initial study seven years ago.

What that means, and this is really the crux of it, is that factors like Quality, Low-Beta, Momentum, Size and even Value were all quite expensive back in 2016. So the outlook for them as profit-producing factors at that point was pretty poor. That was Arnott’s point then, and so it turned out.

But now, he says, they are much cheaper. Compare the two charts and you’ll see that in the US, the factors are cheaper across the board. In Developed Markets (including the UK), Quality, Volatility and Size still look pricey, but Value looks cheaper and Momentum is super-cheap.

It’s a research study that clearly wants to call the bottom for factor investing and promise years of decent returns from here (certainly in the US). It also wants to keep that discussion in the limelight. It’s an interesting read. Not exactly great news for UK factor investors, but an interesting view on how different factors get expensive and cheap over time.

Rob Arnott, Amie Ko, Research Affiliates - Revisiting Our “Horribly Wrong” Paper: That Was Then, This Is Now

If that’s not enough factor investing for you, try this recent podcast (and transcript) from Robeco Asset Management: The best is yet to come for factor investing. Weili Zhou and David Blitz run institutional factor-led funds, and this is 20 minutes of them talking about factor performances over the past couple of years (they’ve been strong) and also mentions the Research Affiliates research (above). It’s also interesting to hear that they are looking at ways that ESG signals might be baked into some of their models.

Highlights from the past week

Klement on Investing - On the importance of long-term earnings forecasts

Joachim Klement quite rightly dislikes long term forecasts. Read his stuff for long enough and that comes across crystal clear. In this short post from earlier in the week, he returns to the perils of estimating long term company growth and how, when so much optimism is priced into shares, it makes it very difficult for them to outperform. On the flip side, when pessimism starts to find its way into prices, then it’s much easier for those shares to beat expectations when companies perform well.

In an added twist, new research into ‘conglomerate’ companies shows that they’re uniquely able to smooth earnings between businesses and create an illusion of stability - so much so that it makes their shares prone to over-valuation and underperformance.

Capital Employed FM - The Advantage of Time with Christopher Godfrey

A big part of the appeal of these fund manager interviews by Jon at Capital Employed is that he speaks to people that you don’t often come across. In this episode he talks to Chris Godfrey, a US money manager who runs a firm called Headwaters Capital Management. His strategy has got a ‘quality compounder’ feel to it, with a concentrated mid-cap growth strategy (currently with 21 holdings) where he’s trying to capture firms early in the growth cycle, especially those with some sort of competitive advantage. As always, there’s a deep dive into two holdings: on this occasion Transcat Inc and UFP Technologies Inc - and it’s interesting to hear some US mid-cap ideas.

The Investors First Podcast - Dan Rasmussen & Bob Elliott - Replicating Private Equity/Hedge Funds in Public Markets

This is pretty heavyweight stuff: Dan Rasmussen is a highly respected value-focused fund manager who runs Verdad, and Bob Elliot is an ex-Bridgewater Associates (Ray Dalio) analyst who is now at Unlimited Funds.

This discussion starts with them talking about their respective ways of taking what private equity and hedge funds strategies do and then applying it to public markets. It then develops into a conversation about strategies, what works, discretionary versus systematic and discipline.

The thrust of this podcast (and quite a few others recently) is that faced with relentless competition from indexing, parts of the professional fund industry (certainly in the US) seem to be gravitating towards private equity models and alpha strategies. Historically, the big frictions in doing this have been costs (PEs and hedge funds charge high fees, which is what indexing alleviates) and capacity constraints (a lot of great alpha strategies stop working when they have too much money to invest). In different ways, Dan and Bob are seeking ways of tackling those obstacles.

Stephen Dover, Franklin Templeton - Quick Thoughts: The dangers of inertia

I’ve covered a few factor investing items this week, so here’s something different. Stephen Dover publishes his commentary in a newsletter on LinkedIn, so if you want his views sent to your email inbox, that’s the way to get it.

This week his article is an interesting take on why asset diversification still makes sense, even after last year’s dual collapse of equities and bonds. He also argues that investors ought to be taking a more active approach to equity selection in the current conditions. There’s an increasingly common argument at the moment that indexing may well be the wrong way to play markets in 2023. That remains to be seen, but in Stephen’s view, index funds are at risk of exposing investors to past winners that are increasingly disappointing on profits.

Thinking & Strategy

Excess Returns

[Podcast] The Art and Science of Intelligent Fund Selection with Joe Wiggins

Klement on Investing

On the importance of long-term earnings forecasts

The Evidence-Based Investor

UK investors are still too heavily concentrated in UK assets

Behavioral Value Investor

The Surprising Ways In Which Losing Money Can Help You Build Wealth

Meb Faber Research – Stock Market and Investing Blog

[Podcast] Episode #465: Jim O’Shaughnessy, OSV – Unleashing The World’s Infinite Potential

Invest Like the Best with Patrick O'Shaughnessy

[Podcast] Carl Kawaja - Dealing with Regime Change - [Invest Like the Best, EP.314]

Institutional Research

Link Group

UK Dividend Monitor Q4 2022

MSCI

The Performance of ESG Indexes: Year in Review

Vanguard

How to hedge against inflation

Artemis

Why this is the perfect environment for stockpickers

S&P Indexology

Style, Size, and Skewness

Securities & Markets

A Long Time In Finance

[Podcast] Barclays: The Bank That Really Wanted to be Big

The Investor Way

[Podcast] E120 - Diageo, Fevertree, Burberry, Ocado, Associated British Foods & Intel

Investors' Chronicle

[Podcast] The Companies and Markets show: Vodafone, GSK and the management merry-go-round

AJ Bell Money & Markets

[Podcast] IMF worries and Terry Smith’s musings

Musings on Markets

Tesla in 2023: A Return to Reality, The Start of the End or Time to Buy and Disagreements and First Principles: The Pushback on my Tesla Valuation

Maynard Paton

[Podcast] BIOVENTIX With Roland Head And Maynard Paton

Money Makers

[Podcast] Weekly Investment Trust Podcast with Jonathan Davis (28 Jan 2023)

Quality Small Caps

[Podcast] Small Caps Podcast with Paul Scott – Episode 4 for 2023