Rules to put you on the path to global tenbaggers…

Rules to put you on the path to global tenbaggers…

Spoiler: A decent set of screening rules can only get you so far

When it comes to stories in the stock market, nothing comes close to capturing the imagination of investors quite like a tale of a ‘multibagger’.

Precise definitions vary, but the term ‘tenbaggers’ was invented by the legendary money manager Peter Lynch. He wrote about them in his book called One Up on Wall Street.

Lynch’s style of growth investing was all about finding shares that were capable of rerating dramatically. Tenbaggers were those that went on to 10-ex your money by increasing in value by 1,000%.

They were hard to come by but they were the kinds of shares that could change your life.

In his book, Lynch stressed the advantages that DIY stock pickers had over professionals. He reckoned that looking out for new trends and products made it possible to find investment ideas long before the Street (or the City) caught on.

In many ways, individual investors still have these advantages. But in the search for multibaggers, data and computing power have taken over as the tools to find patterns in the past that might predict the future.

In late 2022 a global research study was published that looked back over the past 10 years at the common traits of shares that had delivered 1,000%-plus returns.

It was an ambitious endeavour by researchers at an investment house called Jenga Capital, resulting in a 287-page ‘note’ that you can read here.

It wasn’t the first study to try this. Another investment firm, Alta Fox Capital did something similar over a shorter five-year time frame back in 2020, entitled The Makings of a Multibagger. Then there was Christopher Mayer’s book, 100 baggers, that did the same.

An impossible task?

Performance studies like this are fraught with difficulties. The further you look and the broader you reach, the more chance there is of making mistakes.

Reverse engineering performance is prone to survivorship bias. You might be able to create a picture of all the ideal traits that led to outperformance, but what about the same kind of shares that for one reason or another fell by the wayside?

In a global study, not all shares and markets are necessarily accessible to everyone. Things like exchange rate fluctuations, liquidity, market depth and local, or even regional, economic trends can skew the results.

To be fair, this study gives it a go. There are a few countries booted out at the start for having excessive inflation. And the timeframe is carefully chosen to capture the beginning of the market-wide sell off in early 2022. That helpfully dampens down some of the tech sector valuation froth that might otherwise have tainted the results.

The research covers 31st May 2012 to 31st May 2022.

In terms of market cap, they restricted the field to a minimum market cap of $50 million in May 2012 and a minimum market cap of $550 million in May 2022 - providing the scope to capture a 1,000% return.

That minimum market cap rule admittedly screens out micro-caps that can conceivably grow quickly. But stocks that small tend to be uninvestable for many institutions, and thy can be risky.

In total, there were 446 companies in the study that turned out to be tenbaggers.

Past performance is no guide…

The aim was not to find brilliant shares that might continue to perform well. Rather it was about examining the traits of firms that had managed to tenbag, and learn from them.

To organise the findings, businesses were generally classified in one of five different investment styles:

Compounders (classic growth stocks that catch a wave and don’t get things wrong)

Cyclicals (exposed to some bigger trend at the right time)

Turnarounds (where mistakes were made but growth and market leadership were restored)

Stalwarts (well established slow-growers that were cheap to buy)

Special situations (unusual cases like spin-outs)

So what did they find?

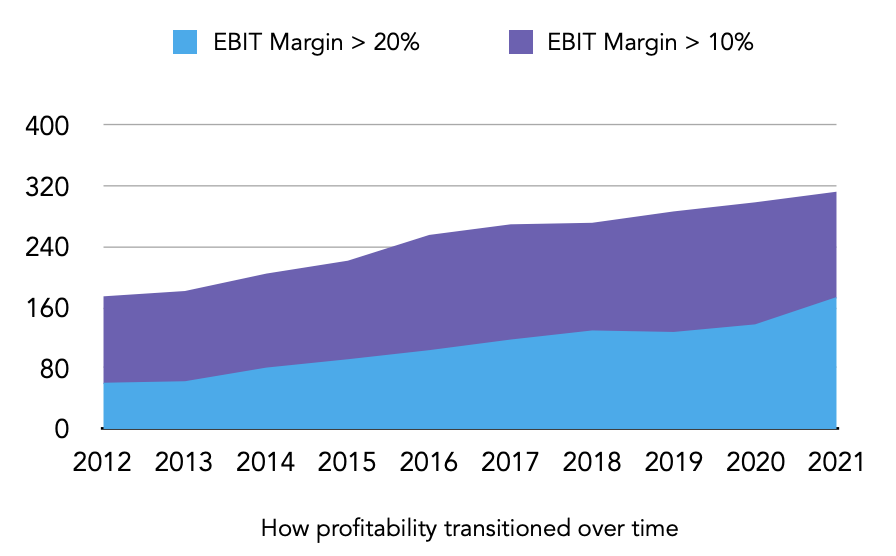

1. Profitable companies had a higher chance of multibagging

Of the 446 companies, 367 of them were profitable from the get-go in 2012. Only 79 either had no revenue at all or were operationally unprofitable. So speculative shares, which sometimes come with lottery-like expectations, had a lower hit rate.

Also of note was that operating profit margins (EBIT) for these firms were important from the start. Nearly half of them had a double-digit margin at the start of the period, and that number grew to 85% by the end.

Margin growth is an important signal - it can happen when earnings grow faster than sales, indicating scale improvements, greater efficiency and pricing power.

2. Earnings growth is not as important as you think

Corroborating other recent studies, this research found earnings growth was important but not as crucial as you might expect. Fewer than a third of firms reporting growth data saw sales grow at more than 20% compounded over the 10 years. In terms of earnings, only 19% of firms reported growth in excess of 20% compounded.

Only 31% of firms in the study managed to compound their earnings at more than 27% a year for 10 years. That suggests that there’s more to tenbaggers than just earnings growth.

3. You don’t have to pay up for outperformance (as long as you can predict the future)

This study used enterprise value (market value plus debt/cash) as the basis for looking back at the role of valuation multiples. In particular it used EV/Revenue and EV/EBIT.

Overall, half of the subset of 1,000% outperformers started the 10 year period with an EV/Revenue below 1x, which is cheap by almost any standard.

On this subject, the researchers found that “the higher the EV/Revenue, the more an investor should demand growth and profitability from companies.”

On EV/EBIT, again nearly half of the profitable companies in the study started with a multiple below 10x, which was notably cheap.

On both measures, multiple expansion played an understandably important role over time. Over the 10 years, 91% of profitable firms saw their EV/Revenue multiple expand, while 72% of profitable firms saw their EV/EBIT multiples expand.

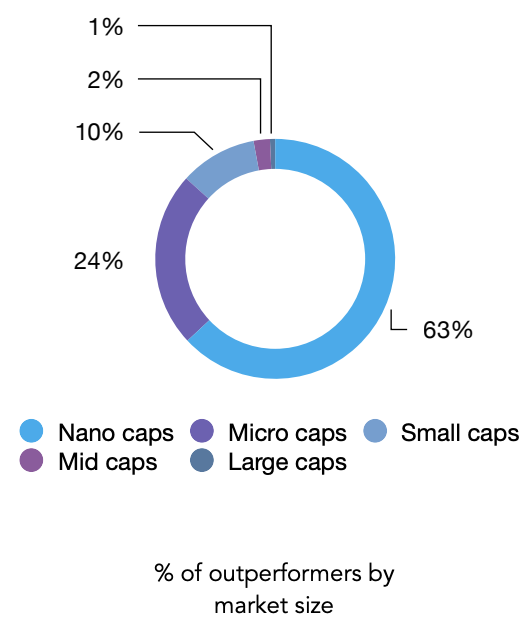

4. Smaller stocks outperform (but we already knew that)

The legendary Jim Slater once wrote that “elephants don’t gallop”, by which he meant that larger stocks find it much harder to deliver the kind of price gains that smaller stocks can.

This research largely supports that view, with nano-cap shares proving to be much the largest source of outperformance relative to the overall market universe (not the subset outperformers in this study).

What are the takeaways?

Well, as the study suggests, the obvious screening rules to learn from the observations are as follows:

EV/Revenue <1.5x

EV/EBIT <10x

Earnings growth of 15% CAGR (assuming you have a crystal ball)

A market capitalisation of less than $300 million

And there’s the problem, … while it’s perfectly possible to go looking for small, cheap profitable companies, the real challenge is in pinning down consistent earnings growth over time.

And it’s not just that…

As the study states, even if you could predict the future, these simple rules would still leave you missing 54% (504 of 935 companies - including nano-caps) that went on to tenbag over the following ten years.

It turns out there are more factors involved than even this solid, simple set of investing rules captures.

So the search for multibaggers goes on. While diving into history can tell us a lot about what’s worked, the fact is that investing is all about the future. Lessons from the past can offer important clues about what is to come, but an open mind and flexibility is also going to be essential.

The full research report can be found here.