Skewed indices and should value investors really care about company size?

It would be easy to look at the 15.7% year-to-date rise on the S&P 500 and start wondering whether 2022 was just another blip.

Okay, last year might have been a longer and deeper blip than some of the S&P’s other setbacks over the past decade or so. Looking back, there was a rough month in early 2016, a dire spell in late 2018, and, of course, Covid shook things up a lot in 2020. But the US large cap index always recovered quickly.

Perhaps this is déjà vu? Perhaps we have just witnessed the biggest BTFD opportunity of all the BTFD opportunities we’ve had since the financial crisis.

Not so fast…

The S&P’s headline performance doesn’t lie (and the Nasdaq is up even more this year, at 32.7%). But the main cause for such a stinging drawdown last year has now become the main reason for the strong performance so far in 2023: the ‘Big 7’.

Alphabet, Amazon.com, Apple, Meta Platforms, Microsoft, NVIDIA, and Tesla have been skewing the index performance like crazy. This note from RBC is only a week old but somewhat dated now given how quickly some of these stocks are moving: Reading between the lines of the stock market rally. But the essence remains: in early June, when the S&P was up 12% (including dividends) year-to-date, the Big 7 were up by an average of 69%.

Because of the market-cap weighting of the S&P (like most other main indices) these substantial moves in a concentrated group of already huge companies have an incredible influence on the index as a whole.

In fact, strip the Big 7 out of the picture, and the S&P is only up by around 2.5% this year.

Here’s how this skewing effect shows up when you look at where S&P 500 returns have come from this year:

Why is it that these large technology stocks are back in demand? Well, at least part of the answer seems to be the explosive popularity of new tech themes like Artificial Intelligence. But there are other, much more regular investment-driven reasons, too:

One of those is simply down to quality. Big 7 tech companies have outperformed the index when it comes to revenue growth, earnings growth, margins and free cash flow trends this year

RBC says positive consensus earnings estimate revisions for these stocks over the past three months have also exceeded the broad index

Plus, RBC points out that the consensus earnings and revenue growth forecasts for the Big 7 over the next 12 months are well ahead of the rest of the S&P 500

With the US Federal Reserve skipping the chance to hike interest rates again this week, there are signs that the end could be in sight for the end-of-cycle inflation battle that has been under way for the past 18 months. While most of the S&P is still subdued on the possibility of recession, big tech is putting 2022 well and truly behind it.

Is smaller really better for value investors?

Sticking with the theme of company size…

There’s a perception in places that value investing in equities really works best in ‘small-caps’. In some ways that’s because of the way style premia, or factors, are sold to investors. If you read the research (and ignore what has happened since 2009), small-caps tend to outperform large caps, and value stocks tend to outperform expensive growth stocks over time (on average).

With those two observations in mind, you don’t have to join too many dots to come up with the idea that small-cap value investing could be a winner. And there’s no argument against it being just that. But at the exclusion of large-caps? Maybe not…

Before getting on to new research from Alpha Architect, it’s worth a reminder that “small-cap” can mean different things in different territories. Here in the UK, small-caps can be anything from around £50 million to £500 million in size.

Over in the States, where most of this kind of academic, factor-focused research is done, small-caps are different. The Russell 3000 index covers around 96% of investable equites in the US. The top third of that - the Russell 1000 - is the large-cap part. The second two-thirds - the Russell 2000 - is seen locally as the small-cap part.

The Russell 2000 comprises stocks spanning market caps from $160 million to $12 billion. The current median market cap is £900 million, which is some way ahead of what most UK investors would think of when it comes to small-caps. So keep that in mind.

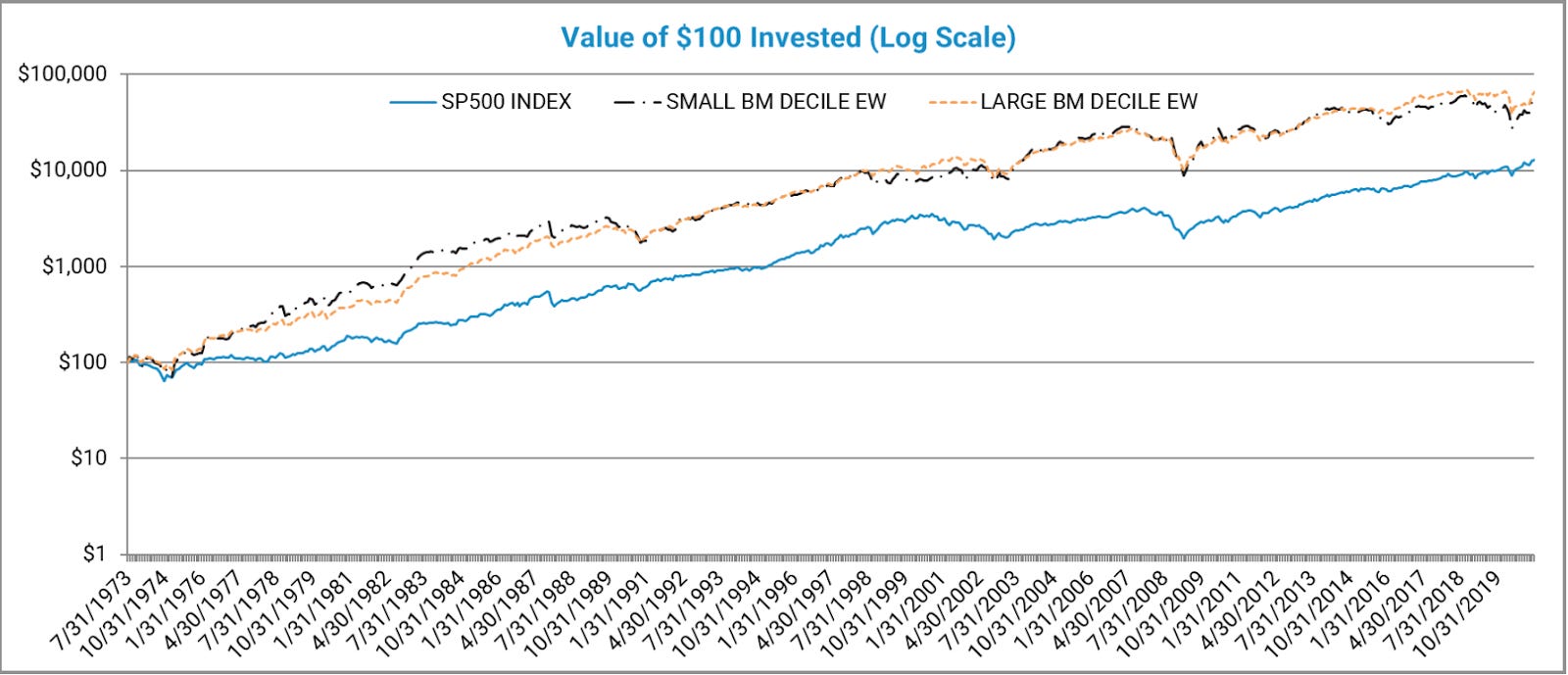

Ironically, this new Alpha Architect research suggests it’s time to stop being concerned with company size, at least when it comes to value investing, because it doesn’t matter - value works everywhere: Long-Only Value Investing: Size Doesn’t Matter!

This chart from Alpha Architect’s research (done by Jack Vogel) shows that large-cap value just pips small-cap value in terms of outperformance over time (on an absolute and risk-adjusted basis).

Alpha Architect reckon that classic value approaches in academic research don’t really mimic the kind of approaches used by regular investors. And when you distil it down, the fact is that “cheap valuation” is far and away the most important consideration in a value strategy, not company size. As they say:

“For example, if you can buy a portfolio with an average P/E of 5x and a market cap of $10B, this will, using historical datasets, outperform a portfolio with an average P/E of 8x and a market cap of $500mm. Why? Size doesn’t drive expected returns — valuation does.”

The takeaway here is that large-cap and small-cap value investing achieve similar returns however you slice and dice the results, and they work internationally too.

Overall…

“The small-cap sacred cow has been slaughtered… if you love small-cap investing, you should really like equal-weight large-cap value investing — similar expected returns with almost no holdings overlap (which may provide diversification opportunities).”

Have a great weekend!

Thinking & Strategy

Macro Ops

Randy McKay’s Trading Strategy Explained

Behind the Balance Sheet

[Podcast] #23B The Best Selling Author Part 2

The Investor Way

[Podcast] E139 - Ben Bennett Interview Part 2 (Twitter - @Value_OnePagers)

The Long View

[Podcast] Jeremy Schwartz: Why Stocks Are Good Inflation Hedges

Joachim Klement

A thought about bank profitability

Morgan Housel

Compounding Optimism

Lyn Alden

Do High Interest Rates Fix High Inflation?

A Wealth of Common Sense

This is Why You Stay the Course

Behavioral Value Investor

Lessons From Warren Buffett’s See’s Candies Acquisition

Securities & Markets

Twin Petes Investing

Podcast no.103 with LIVE in person video

Investors' Chronicle

[Podcast] The Companies and Markets show: Housebuilders, small caps and passive funds

UK Dividend Stocks Blog

Is it time to buy shares in Robert Walters?

Maynard Paton

[Podcast] BELLWAY, LUCECO And SUPERDRY With Roland Head, Mark Simpson, Bruce Packard And Maynard Paton

Money Makers

Weekly Investment Trusts Podcast - with Russell Napier and Janette Rutterford (10 Jun '23)