Strategy Checklists, hit rates vs. payoffs, Todd Combs and when to invest - the best investing blogs and podcasts from the past week

Just a quick note to say I’m introducing something new at Fully Invested…

As part of my day job I spend a lot of time thinking and writing about different strategies for investing in the stock market. I want to take that further and build a library of strategy checklists that answer the questions that I think are likely to be on the minds of investors. So I’ve started doing it.

I have begun with three (links below), and future checklist articles will come to you direct. I hope you find them useful. Feel free to message me with any ideas, suggestions or anything else.

How to find shares that can defend themselves (and you) you against inflation and recession

How to find shares with high dividend yields (that won’t let you down)

Friday emails will stay as they are, and with that in mind…

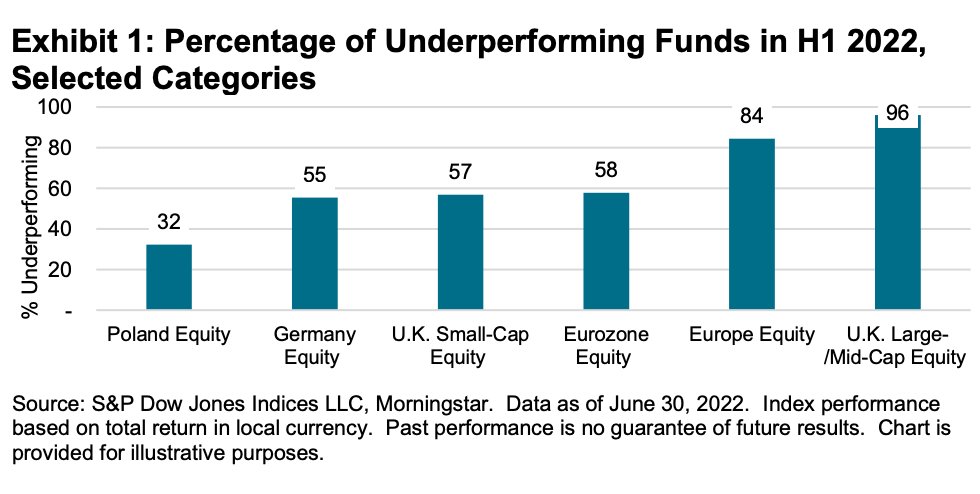

In a year when stock markets have been tough on investors, you could say it’s a bit mean to pick holes in the performances of some of them. But when the S&P SPIVA Scorecards were published in September it was surprising to see that 96% of UK funds in the large-/mid-cap category had underperformed in the first half of 2022.

To clarify, SPIVA stands for “S&P Indices Versus Active Funds”. So this is S&P (the index company) comparing active manager performance around the world to their relevant benchmarks (you can check it out here). For what it’s worth the research consistently finds that active funds lag their benchmarks all over the world.

Here in the UK, S&P’s large-/mid-cap benchmark was actually the only index showing a positive return in the first half. That was because the country’s large-caps are heavily weighted to energy and resources sectors, which held up well.

Nonetheless, nearly all the UK funds in that category underperformed the benchmark. Why? Well it seems that one reason at least is that some “might” be dipping their toes into small-caps to try and spice up their returns.

If that is the case (and S&P suggests it is) not only would it be ridiculous, but it would also have been a terrible decision by those fund managers given how badly small-caps have performed this year (this is a couple of months old now, but here's the full note).

Back to the present, and on the subject of fund manager decisions, there is an interesting article here on the difference between hit rates and payoffs when it comes to judging investing skill: Manager Selection: The Power of Payoff.

A hit rate is basically a success rate. Get more decisions right than wrong and you should come out on top. In that respect it’s well suited to factor investing where a tilt to styles like value or momentum aims to scrape the factor premium rather than trying to be clever with stock picking.

But this research - by Essentia Analytics, a firm that specialises in measuring fund performance - suggests that stock picking skill is better tracked by looking at payoffs.

Payoffs are a measure of whether the profits from good decisions are greater than the losses from bad decisions. Those decisions include what and when to buy, as well as when to hold and sell. A small number of big payoffs can easily compensate for several poor decisions. The theory is that focusing on payoffs helps to strip out the role of luck when it comes to figuring out investor skill.

The problem of course, is that whether you're using hit rates or payoffs, studying past performance in fund management is a notoriously bad way of predicting future winners.

Ideally, it’s preferable to be looking at process rather than outcomes when it comes to these things. And on that note, this article from Joachim Klement this week is another reminder of just how hung up retail investors are when it comes to using past performances as a guide to choosing fund managers: What matters for fund investors is not what should matter.

Top posts from the past week

Investment Management Insights - Graham & Dodd Annual Breakfast 2022

It’s hard to scroll through Twitter these days without tripping over a new Warren Buffett-related article, but this is worth a look. Todd Combs is the CEO of GEICO, the all important insurance business owned by Buffett’s Berkshire Hathaway. He’s also the group’s investment manager. He was recently the guest speaker at the Graham & Dodd Annual Breakfast, moderated by Michael Mauboussin. This write up gives a genuinely interesting insight into some of the thinking that goes on between Combs, Buffett and his business partner, Charlie Munger. There are loads of highlights but one comment that did strike me was how little concern any of them have about macro conditions, inflation or whatever lies in store in the short term. Important lesson there, I think.

Howard Marks, Oaktree Capital - What Really Matters?

The crux of this 7,300 word note from Howard Marks of Oaktree Capital is summed up in a bullet point towards the end: “Forget the short run – only the long run matters”. I have no idea how Oaktree has fared through this year, but I imagine quite a few of its clients are rattled. So it makes sense that Marks has arrived to try and calm nerves. It’s actually a great summary of the best parts of other memos this year, with a focus on the pointlessness of worrying about macro, of forecasting, of thinking short term, of over trading and worrying about volatility - all the things that investors do. Sadly there’s no audio option with this latest article, but it’s definitely worth a read.

Excess Returns Podcast - A Common Sense Approach to Markets with Ben Carlson

Ben Carlson is usually found writing at his blog, A Wealth of Common Sense. He’s been doing that for nearly a decade, and in between times became a director at Ritholtz Wealth Management. He’s very much a voice of reason, and that comes across in this podcast interview with him. From a selfish point of view, I was quite pleased that they got him talking about his writing process. But obviously, they cover a lot of ground in terms of market and economic conditions. As a firm, I believe Ritholtz has a preference for global, low cost diversified approaches and bristles a bit at the idea of stock picking for most investors. That said, Carlson’s quite pragmatic on issues like factor investing and trend following. Indeed, his closing remarks wrap things up quite well: find a strategy that suits you and you can live with, and stick with it regardless of whatever anyone else is doing.

Monevator - Is now a good time to invest?

There’s a bit of a theme going on this week. Faced with so much bad news it would be easy to talk yourself out of the stock market, and many have. And while it’s certainly possible to talk at length about all the theoretical reasons why you should keep calm and carry on, sometimes that logic wears a bit thin. So this article from Monevator is just what the doctor ordered. Some punchy charts and a dressing down. Historically, harsh bear markets are always followed by big recoveries - but by the time they happen, many of us are curled up in a ball. If there was ever a time to “upgrade your mental firmware from the basic fear and greed package” this is it.

Have a great weekend!

Ben

Thinking & Strategy

A Long Time In Finance

[Podcast] The City Contra Mundum

We Study Billionaires - The Investor’s Podcast Network

[Podcast] Classic 22: Life and investing w/ Mohnish Pabrai

Behavioural Investment

What Next for Defensive and Cautious Investors After a Torrid 2022?

Meb Faber Podcast

[Podcast] Robeco – The Cross-Section of Stock Returns before 1926 (and beyond) (The Best Investment Writing Volume 6)

Investor Amnesia

How Intangible Assets Shape Markets

Neckar's Minds and Markets

The Hustler: Lessons from a Young Warren Buffett

Institutional Research

Premier Miton

Distinct changes bring about distinct opportunities

Franklin Templeton

Economic trends and investment themes for 2023 and beyond

Artemis

Creative destruction: Out of failure, new opportunities for smaller companies...

Schroders / The Value Perspective

Current market turmoil has its roots in the stability of the past decade

AQR Capital

Trend-Following: Why Now? A Macro Perspective

Alpha Architect

Active Managers are Subject to the Same Biases as Individual Investors

Securities & Markets

The Investor Way

E110 - Taylor Wimpey, M&S, AutoTrader, Young & Cos Brewery, Haleon & Disney

MSCI

The Rise and Fall of Big Tech

Maynard Paton

[SharePad] Small-Cap Spotlight Report: TRUSTPILOT

[Podcast] CITY OF LONDON INVESTMENT With Mark Atkinson And Maynard Paton

Tom Stevenson, Fidelity International

It’s grim right now, but 2023 is already looking brighter

Quality Small Caps

[Podcast] Small Caps Podcast with Paul Scott – Episode 21